Anúncios

Financial distress can strike anyone, but understanding your options between loan modification and default can mean the difference between recovery and long-term financial damage.

When mortgage payments become overwhelming, homeowners face a critical crossroads that will shape their financial future for years to come. The pressure of missed payments creates anxiety, sleepless nights, and mounting stress as bills pile up and creditor calls increase. However, this challenging moment also presents an opportunity to make strategic decisions that can preserve your financial health and keep you in your home.

The path you choose—whether pursuing a loan modification or allowing your account to fall into default—will have profound implications on your credit score, homeownership status, and overall financial well-being. This comprehensive guide explores both options in depth, helping you understand the real consequences, hidden opportunities, and practical steps to navigate this difficult financial terrain with confidence and clarity.

💡 Understanding Loan Modification: Your Financial Lifeline

A loan modification represents a formal agreement between you and your lender to permanently change the original terms of your mortgage. Unlike refinancing, which replaces your existing loan with a new one, modification alters your current loan structure to make payments more manageable within your present financial circumstances.

Lenders offer modifications because foreclosure is expensive and time-consuming for them as well. The process typically costs lenders between $50,000 and $70,000 per foreclosure, including legal fees, property maintenance, and lost interest payments. This creates a strong incentive for lenders to work with struggling borrowers who demonstrate genuine commitment to staying in their homes.

Common Loan Modification Strategies That Work

Loan modifications can take several forms, each designed to address different financial hardships. The most common modification types include interest rate reductions, which lower your monthly payment by decreasing the percentage you pay on the principal balance. Some borrowers see rates drop from 6% to 3%, resulting in hundreds of dollars in monthly savings.

Term extensions stretch your loan over a longer period—perhaps from 30 years to 40 years—reducing monthly payments by spreading the debt across more time. While this increases the total interest paid over the loan’s life, it provides immediate monthly relief when cash flow is tight.

Principal forbearance programs allow lenders to set aside a portion of your loan balance as non-interest-bearing, reducing your payment calculation base. This deferred amount typically comes due when you sell the property, refinance, or pay off the loan, but it doesn’t accrue interest in the meantime.

Principal reduction, though less common, involves the lender actually forgiving a portion of what you owe. This approach became more prevalent during the 2008 financial crisis but remains rare today, typically reserved for situations where the home’s value has dropped significantly below the loan amount.

🏠 The Default Path: Understanding What You’re Really Facing

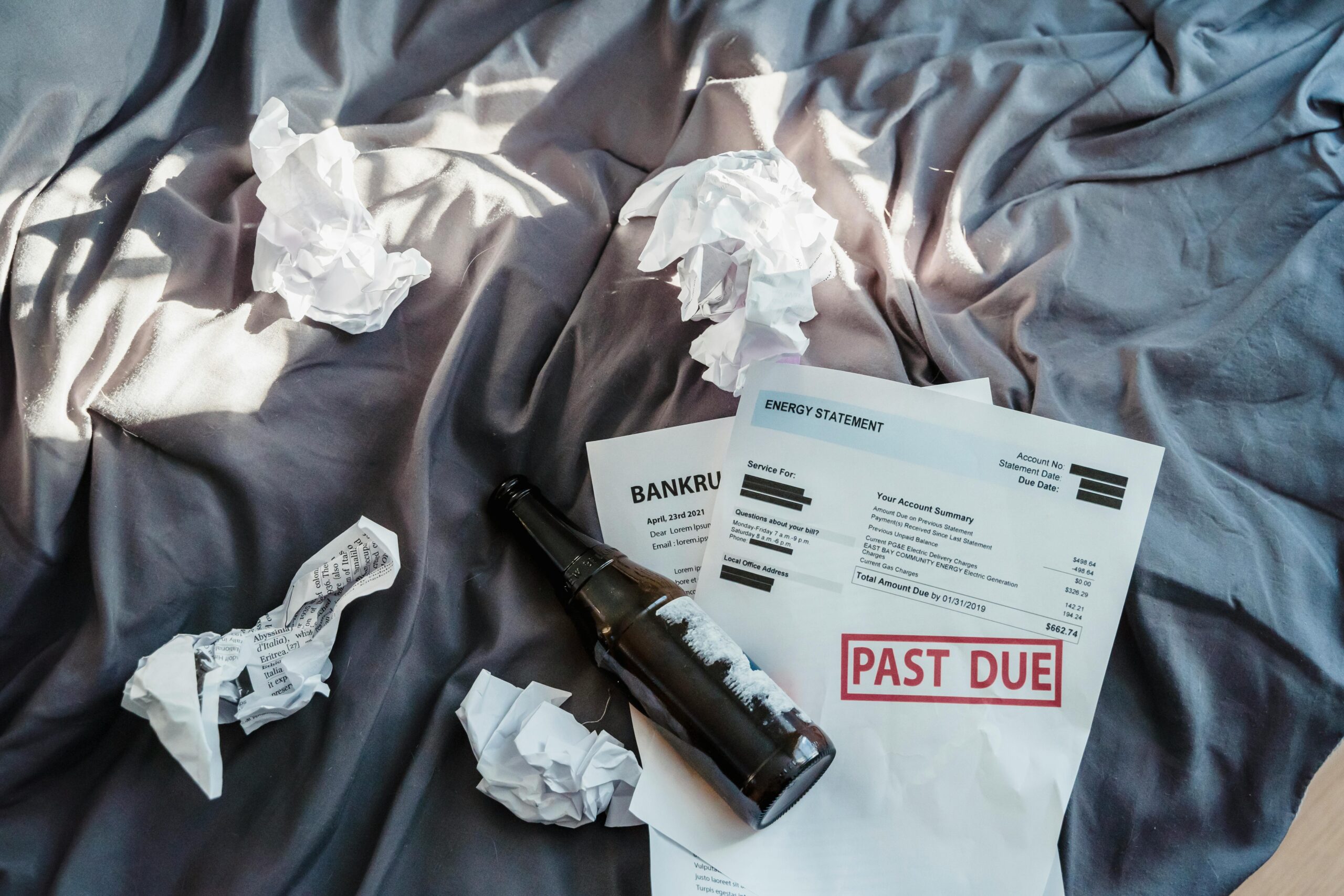

Default occurs when you fail to meet the contractual obligations of your mortgage agreement, typically by missing payments. What many homeowners don’t realize is that default isn’t a single event but rather a progressive process with escalating consequences at each stage.

The first missed payment triggers late fees and concerned communication from your lender. By the second missed payment, your account officially enters delinquency status, and your credit score begins suffering measurable damage. After three consecutive missed payments, most lenders initiate the pre-foreclosure process, sending formal notices and potentially beginning legal proceedings.

The Cascading Consequences of Default

The immediate impact of default centers on your credit score, which can drop 100 to 160 points after a single 30-day late payment. A 90-day delinquency can decrease scores by 200 to 300 points, devastating your borrowing capacity for years to come. This damage affects far more than your ability to get another mortgage—it influences auto loan rates, credit card approvals, apartment rental applications, and even job prospects in some industries.

Beyond credit damage, default puts your home at direct risk. The foreclosure process varies by state, taking anywhere from several months to several years, but the outcome remains constant: loss of your property. Judicial foreclosure states require court proceedings, offering more time but also creating public records of your financial difficulties. Non-judicial foreclosure states allow faster processes with fewer legal protections for homeowners.

The emotional and psychological toll of default shouldn’t be underestimated. The stress of facing foreclosure affects mental health, family relationships, and physical well-being. Children in households facing foreclosure show increased behavioral problems and academic difficulties, while adults experience higher rates of anxiety, depression, and health issues.

📊 Comparing the Real Costs: A Side-by-Side Analysis

| Factor | Loan Modification | Default/Foreclosure |

|---|---|---|

| Credit Score Impact | 20-100 point decrease (temporary) | 200-300+ point decrease (lasting 3-7 years) |

| Home Retention | High probability with successful modification | Guaranteed loss through foreclosure |

| Monthly Payment | Reduced to affordable level | Eliminated (but no home ownership) |

| Long-term Cost | Potentially higher total interest | Lost equity plus rental costs |

| Future Borrowing | Possible within 1-2 years | Severely limited for 3-7 years |

| Tax Implications | Possible forgiveness taxability | Deficiency judgments and forgiveness taxes |

This comparison reveals that while default might seem like an escape from overwhelming payments, it actually creates longer-lasting and more severe financial consequences than pursuing modification alternatives.

🎯 Qualifying for Loan Modification: Meeting Lender Requirements

Securing a loan modification requires demonstrating genuine financial hardship while also proving your ability to make modified payments. Lenders aren’t looking for perfect financial situations—they’re evaluating whether modification creates a sustainable path forward that’s better than foreclosure.

Acceptable hardship reasons include job loss or income reduction, medical emergencies or unexpected healthcare costs, divorce or separation, death of a spouse or co-borrower, and natural disasters affecting your property or income. Some lenders also accept military service deployment, business failures, and increased expenses due to caring for elderly parents or disabled family members.

Documentation That Strengthens Your Modification Application

Successfully obtaining a modification depends heavily on thorough documentation. Your application package should include recent pay stubs covering the past two months, tax returns from the previous two years, bank statements showing all accounts for the past two to three months, and a detailed hardship letter explaining your specific circumstances.

The hardship letter deserves special attention as your opportunity to present your case personally. Effective letters explain exactly what caused your financial difficulty, demonstrate that the situation was beyond your control, show steps you’ve taken to improve your finances, and express your commitment to keeping your home while making modified payments.

Additional supporting documents might include medical bills, divorce decrees, unemployment benefit statements, disability documentation, or employer letters confirming reduced hours or position elimination. The more comprehensive your documentation, the stronger your application becomes.

⚖️ Strategic Decision-Making: Choosing Your Path Forward

The decision between pursuing modification and accepting default isn’t always straightforward. Several key factors should influence your choice, starting with your emotional attachment to the property and community. If your home represents significant family history, proximity to excellent schools, or community ties that matter deeply to you, fighting for modification makes emotional and practical sense.

Your equity position plays a crucial role in this decision. If you’ve built substantial equity—typically 20% or more—walking away through default means losing that accumulated wealth. However, if you’re significantly underwater (owing more than the home’s worth), the calculation changes, though modification might still offer the better long-term outcome.

When Default Might Be the More Practical Option

Certain situations genuinely warrant considering default as the more strategic path. If you’ve experienced permanent income loss with no realistic prospect of affording even modified payments, continuing to struggle delays the inevitable while draining remaining resources that could rebuild your financial life elsewhere.

When your mortgage significantly exceeds your property’s value—being 30% or more underwater—and the local market shows no signs of recovery, you’re essentially paying premium prices for a devalued asset. Though painful, strategic default might preserve resources for a fresh start.

Job relocation requirements sometimes make keeping the property impractical, particularly in markets where selling would require bringing substantial cash to closing. If maintaining the property prevents you from pursuing essential career opportunities, default might be the pragmatic choice, though a short sale should be explored first as a less damaging alternative.

🛡️ Protecting Yourself During the Modification Process

Navigating loan modification requires vigilance against scams and predatory practices. Unfortunately, desperate homeowners become targets for modification frauds that promise guaranteed approval in exchange for upfront fees. Legitimate housing counselors and attorneys can help with modifications, but they shouldn’t guarantee outcomes or demand large advance payments.

Working with HUD-approved housing counseling agencies provides free or low-cost assistance from qualified professionals. These nonprofit organizations offer objective guidance without the conflicts of interest that affect some for-profit modification companies. Find approved counselors through the HUD website or by calling their helpline.

Maintaining Communication With Your Lender

Consistent, proactive communication with your lender dramatically improves modification success rates. Don’t avoid their calls or letters—lenders interpret silence as lack of interest in resolving the situation. Instead, document every conversation, including the date, time, representative’s name, and discussion summary.

Submit requested documentation promptly and completely. Incomplete applications get rejected routinely, forcing you to restart the process and losing valuable time. Create copies of everything you submit and use certified mail or email with read receipts to prove delivery.

If your initial modification application gets denied, request a specific explanation and ask what additional information might support approval. Many successful modifications require multiple submissions as borrowers address lender concerns and strengthen their applications.

💰 Financial Recovery After Modification or Default

Whether you successfully modify your loan or ultimately face default, rebuilding your financial foundation requires deliberate strategy and patience. Post-modification, your priority should be consistently making the new payments on time while gradually rebuilding your emergency fund to prevent future payment interruptions.

Budget adjustments become essential—the circumstances that led to financial hardship often require permanent lifestyle changes. Track expenses meticulously for at least three months to identify reduction opportunities. Small recurring expenses often accumulate to significant amounts that could strengthen your financial buffer.

Rebuilding Credit After Financial Setbacks

Credit recovery following modification happens relatively quickly if you maintain perfect payment history on your modified loan. The modification itself may note “partial payment agreement” on your credit report, but consistent on-time payments gradually improve your score. Most borrowers see substantial score recovery within 12-24 months.

After default and foreclosure, credit rebuilding requires more time and strategy. Begin with secured credit cards that require deposits but report to credit bureaus. Use these cards for small recurring expenses, paying the balance in full monthly. This establishes positive payment history without risking unmanageable debt.

Becoming an authorized user on a responsible family member’s established account can also help, though this strategy’s effectiveness has diminished under recent credit scoring model changes. Focus primarily on establishing your own positive payment patterns across multiple account types over time.

🔑 Alternative Solutions Beyond Modification and Default

Several other options exist between modification and foreclosure that might better fit your specific situation. Short sales allow you to sell your property for less than the mortgage balance with lender approval, avoiding foreclosure while acknowledging you can’t maintain the loan. Though your credit score still suffers, the impact is less severe than foreclosure, and you might negotiate release from deficiency balance claims.

Deed in lieu of foreclosure involves voluntarily transferring your property title to the lender, who agrees not to pursue foreclosure. This option works best when you have no equity and can’t sell the property, providing a more dignified exit than foreclosure while potentially avoiding deficiency judgments.

Forbearance agreements temporarily reduce or suspend your payments while you recover from short-term hardships. Unlike modifications, forbearance doesn’t permanently change your loan terms—you’ll need to repay the suspended amounts later through lump sum, repayment plan, or loan modification. Forbearance works well for temporary setbacks like medical leave or brief unemployment when you expect income recovery.

📈 Long-Term Financial Planning After Crisis Resolution

Emerging from mortgage crisis—whether through modification, default, or alternative resolution—provides valuable perspective for stronger long-term financial planning. This experience, though painful, offers lessons that can prevent future crises and build lasting financial resilience.

Emergency fund development becomes non-negotiable. Financial experts traditionally recommended three to six months of expenses, but experiencing mortgage hardship reveals the wisdom of six to twelve months for homeowners. Build this fund gradually, starting with $1,000, then progressing to one month’s expenses, and continuing until you reach your target.

Income diversification protects against future employment disruptions. Consider developing skills for freelance work, creating passive income streams through investments or creative projects, or building side businesses that could sustain you during employment gaps. Multiple income sources provide security that single employment can’t match.

Housing Payment Ratio Reconsideration

Traditional lending guidance suggests housing payments shouldn’t exceed 28-31% of gross monthly income, but conservative financial planning argues for 25% or less. This lower ratio provides cushion for unexpected expenses, income disruptions, and wealth-building activities like retirement savings and investment.

When you eventually move to your next home—whether after successfully completing modification or rebuilding after default—apply the lessons learned by choosing affordability over maximum approval amounts. Lenders approve loans based on their risk tolerance, not your financial goals. Choose payments that leave substantial room in your budget for savings, emergencies, and life’s unpredictable expenses.

🌟 Taking Action: Your Next Steps Toward Financial Stability

If you’re currently facing mortgage difficulties, taking immediate action dramatically improves your outcome regardless of which path you ultimately choose. Contact your lender today—not tomorrow or next week—to discuss your situation and available options. Many lenders offer internal modification programs beyond federal programs, and you’ll never discover these options without asking.

Simultaneously, schedule appointments with a HUD-approved housing counselor and potentially a bankruptcy attorney (even if you’re not considering bankruptcy, these attorneys understand all foreclosure alternatives and can provide valuable perspective). These consultations typically cost nothing or very little while providing professional guidance worth thousands of dollars.

Gather your financial documentation immediately, creating a complete picture of your income, expenses, assets, and debts. This preparation accelerates any application process and demonstrates seriousness to lenders evaluating your modification request. Organization signals responsibility—a quality lenders want to see in borrowers they’re considering helping.

Remember that financial setbacks don’t define your worth or permanently determine your future. Millions of Americans have faced similar challenges and emerged with stronger finances and clearer priorities. The key difference between those who recover quickly and those who struggle for years often comes down to facing the situation directly, making informed decisions, and taking consistent action toward resolution.

Your home represents more than a financial asset—it’s where you build memories, raise families, and create stability. Fighting for that through loan modification makes sense when realistic. However, if modification isn’t viable, accepting reality and strategically moving forward prevents prolonged suffering and positions you for faster recovery. Either way, informed action beats paralysis every time, and your financial freedom depends on decisions you make today.